Editor of China Economic Net: On September 21, Zhejiang Taihua New Materials Co., Ltd. (hereinafter referred to as “Taihua New Materialsâ€) officially listed on the main board of the Shanghai Stock Exchange, stock code: 603055. The lead underwriter of Taihua New Materials is CITIC Securities. The company is mainly engaged in the R&D, production and sales of nylon filament, nylon grey fabric and nylon finished fabric. It is one of the few nylon industrial chain manufacturers in China. The main products are nylon filament, nylon grey fabric and nylon finished fabric, in addition to producing a small amount of polyester products. The total amount of funds raised was 6.2259 million yuan, after deducting the issuance expenses of 67.59 million yuan. The net proceeds raised this time were 55.5 billion yuan for the annual dyeing of 80 million meters of high-grade differentiated functional nylon fabric expansion project, and finishing 34.5 million meters of high-grade processing after the year. Special functional fabric expansion project, new fiber and fabric technology research and development center project.

According to public information, on June 9, 2017, Taihua New Materials released the latest prospectus. The first application was approved on August 9. On September 11, Taihua New Materials opened the subscription, the purchase code is: 732055, the purchase price: 9.21 yuan, the single account purchase limit of 20,000 shares, the purchase quantity 1000 shares multiple times. The number of shares issued this time was 67.6 million shares, and the final number of online issuances was 60.84 million shares, accounting for 90% of the number of shares issued this time. The stock issuance price is 9.21 yuan / share, and the price-earnings ratio is 22.97 times. More than 123,000 shares were abandoned by investors, of which online investors abandoned 90,633 shares and offline investors abandoned 8,189 shares. The final rate of online issuance was 0.04483893%. From the stock price trend, since the listing on September 21, Taihua New Materials has been trading for seven consecutive trading days. As of the close of November 2, the stock reported 21.06 yuan.

According to the prospectus, from 2012 to January to January 2017, the company realized operating income of 1,706,812,200 yuan, 1,850,205,100 yuan, 1,941,721,100 yuan, 1,89,691,100 yuan, 2,243,180,200 yuan, 1,03,371,400 yuan. The net profit was RMB 134,630,000, RMB 11,554,900, RMB 80,640,300, RMB 4,139,900, RMB 22,755,200 and RMB 20,114,800. The net cash flow from operating activities was 187,883,300 yuan, 11,575,300 yuan, 214,431,900 yuan, 472,443,100 yuan, 791,921,900 yuan, and 14,462,600 yuan.

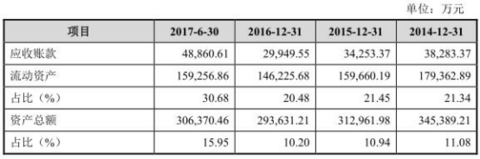

From 2012 to January-June 2017, the company's net accounts receivable were 244,506,300 yuan, 287,321,100 yuan, 382,823,700 yuan, 342,253,700 yuan, 294,495,500 yuan, and 486,606,100 yuan. The proportion of accounts receivable to current assets was 14.88%, 15.14%, 21.34%, 21.45%, 20.48%, and 30.68%, respectively. The accounts receivable turnover rate (times) were 7.87, 6.97, 5.80, 5.23, 6.99, and 6.62, respectively. The book value of inventories was 786,698,600 yuan, 890,958,400 yuan, 892,428,800 yuan, 710,806,500 yuan, 597,365,500 yuan, and 666,958,900 yuan, accounting for 47.90%, 47.21%, 49.77%, 44.97%, 40.85% of current assets, respectively. 41.97%. The inventory turnover rate (times) was 1.70, 1.72, 1.72, 1.86, 2.55, 2.85, respectively. The gross profit margin of the company's main business was 23.95%, 21.40%, 20.07%, 20.67%, 25.02%, 30.62%.

From 2012 to January-June 2017, the total liabilities of the company were 2,245,590,500 yuan, 2,258,888,100 yuan, 2,923,828,200 yuan, 1,942,281,900 yuan, 1,53,806,500 yuan, and 1,497,183,300 yuan. Current liabilities were RMB 205,188,000, RMB 2,819,696,200, RMB 2,095,528,300, 1,841,537,700, 1,512,742,200, and 1,454,470,000 yuan respectively. The gearing ratio (consolidated) was 69.95%, 70.06%, 66.39%, 62.0% 6, 52.38%, and 48.89%, respectively.

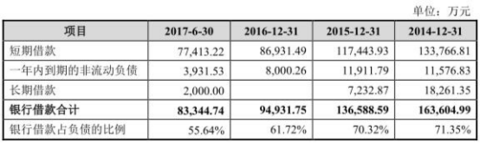

In recent years, corporate bank borrowings have remained at a relatively high level. From 2014 to January to January 2017, bank loans were 1,636,409,900 yuan, 1,365,885,900 yuan, 943,931,500 yuan and 833,344,400 yuan respectively, and the corresponding interest expenses were 11,828,900 yuan respectively. , 9,420.01 million yuan, 5,941,770 yuan and 20,154,200 yuan, the amount is higher. The proportion of corporate bank borrowings to total liabilities was 71.35%, 70.32%, 61.72% and 55.64%, respectively, which accounted for a relatively high proportion and was a major component of the company's liabilities.

The above data shows that in 2016, the company's total liabilities were 1.5 billion yuan, of which bank loans were 900 million yuan, accounting for 61.72% of the total liabilities. The company's 2014-2016 interest expense totaled 271 million yuan.

It is calculated that the company's operating income in 2016 was 2.244 billion yuan, an increase of 347 million yuan from 1.897 billion yuan in 2015, an increase of 18.29%. In 2016, the net profit of 228 million yuan was 188 million yuan more than the 401 million yuan in 2015, an increase of 449.71% over the same period. In 2016, the company's net profit growth rate far exceeded the growth rate of revenue.

The Board of Directors of the China Securities Regulatory Commission also inquired about Taihua New Materials in the announcement of the results of the 120th meeting in 2017: During the reporting period, the net profit of the issuer fluctuated greatly, and the net profit continued to decline sharply from 2013 to 2015. The specific reasons and rationality of the net profit increase of 450% when the income only increased by 18.29%; (4) further explain the issuer by combining the current orders, the operation in 2017, the macro economy and the development of the upstream and downstream industries. Whether the operating profit in the year of listing fell by more than 50% from the previous year or the forecast basis and reason for the loss in the year of listing, whether it is prudent and reasonable, and whether the relevant risks are fully disclosed.

According to the "International Finance News" report, industry insiders said that the performance of Taiwan's new materials has soared, but the improvement of actual operating conditions is not obvious. If it is successfully listed, it is likely to face the risk of short-term performance.

The prospectus also shows that compared with comparable companies in the same industry, the company has not made provision for bad debts for accounts receivable within 6 months. As of the end of 2016, the book value of accounts receivable of Taihua New Materials within 6 months was 275.48 million yuan. If the provision for bad debts was made at 5%, the net profit would be reduced by 13.5 million yuan.

According to the prospectus, nylon filament, nylon grey fabric and nylon finished fabric are the main products of the company. The proportion of the three types of products in the main business income remains above 80%. From 2012 to January-June 2017, the average sales price of nylon filament yarns of the company was 3.04 yuan/kg, 2.63 yuan/kg, 2.34 yuan/kg, 2.16 yuan/kg, 1.87 yuan/kg, 2.20 yuan/kg. The average sales price of nylon grey cloth is 4.39 yuan / meter, 4.23 yuan / meter, 4.14 yuan / meter, 3.77 yuan / meter, 3.66 yuan / meter, 4.31 yuan / meter. The average selling price of nylon finished fabrics was 9.39 yuan / meter, 9.75 yuan / meter, 10.20 yuan / meter, 10.09 yuan / meter, 10.35 yuan / meter, 11.20 yuan / meter.

According to Hexun.com, Taihua New Materials and its holding subsidiaries currently have 4 major lawsuits. Among them, 3 cases were dunning suits for accounts receivable between Taihua New Materials and customers, involving a total of approximately RMB 3,148.45 million in non-returnable principal and interest. Shi Qingdao, the company's actual controller, also involved 4 joint guarantee lawsuits, which required a large amount of joint guarantee responsibility, involving an amount of about 31,729,700 yuan.

In the third quarter of 2017, Taihua New Materials reported that from January to September 2017, the company achieved operating income of 2.018 billion yuan, and the net profit attributable to shareholders of listed companies was 272 million yuan. The net cash flow from operating activities was 342 million yuan, accounts receivable was 405 million yuan, and inventory was 633 million yuan. The total liabilities were 1.311 billion yuan.

In response to the above content, China Economic Net interviewed Taihua New Materials Secretary, but did not receive a reply as of press time.

The company is engaged in nylon weaving business. It is a foreign-invested enterprise. One of the actual controllers is Hong Kong residents.

According to the prospectus, the company has been engaged in the nylon weaving business since its establishment. It is mainly engaged in the R&D, production and sales of nylon filament, nylon grey fabric and nylon finished fabric. It is one of the few nylon industrial chain manufacturers in China. The main products are nylon filament, nylon grey fabric and nylon finished fabric, in addition to producing a small amount of polyester products.

The controlling shareholder of the company is Fuhua Global, which directly holds 211,134,900 shares of the company, accounting for 41.90% of the company's total share capital before the issuance. Fuhua Global was established on July 28, 2003. The authorised share capital is HK$10,000, which is mainly engaged in investment business. Shi Xiuyou holds a 100.00% stake in Fuhua Global.

The company's actual controllers are Shi Xiuyou and Shi Qingdao's younger brothers, who hold 211,134,900 shares and 124,065,500 shares respectively through Fuhua Global and Chuangyou Investment, accounting for 41.90% and 25.85% of the total share capital before the issuance, respectively. The total holding of the company's 325,314,400 shares, accounting for 67.76% of the total share capital before the issuance. Shi Xiuyou, Hong Kong identity card number is K5126xxx. The current company director. Shi Qingdao, Chinese nationality, without permanent residency abroad, served as chairman of the company.

The company was established by Taihua Special Textiles (Jiaxing) Co., Ltd. as a whole. The “Zhejiang Business Letter†issued by the Zhejiang Provincial Department of Commerce on September 6, 2011

No. 191 “approved, agreed to the application for the overall change of Taihua Textile. According to the “Audit Report†issued by Zhonghui, Taihua Textile's net assets as of July 31, 2011 was RMB 547,272,200, and the shares were converted at a ratio of 1:0.822027. The overall change was to establish a foreign-invested joint-stock company. The share capital of the changed company was 450 million shares, and the par value of each share was 1 yuan. The net assets exceeding the share capital were included in the capital reserve. On September 7, 2011, the Zhejiang Provincial People's Government The new "Taiwan, Hong Kong and Macao Overseas Investment Enterprise Approval Certificate of the People's Republic of China" was issued. On September 26, 2011, the Zhejiang Administration for Industry and Commerce approved the application for the overall change of Taihua Textile to a joint stock limited company, and issued a new "Enterprise. Legal person business license. The company name was changed to Zhejiang Taihua New Materials Co., Ltd., with a registered capital of RMB 450 million and registration number 330400400006900.

Fuhua Global is a foreign-invested shareholder, holding 211,134,900 shares, accounting for 41.90% of the company's total share capital before the issuance.

According to the National Economic Industry Classification (GB/T 4754-2011) issued by the National Bureau of Statistics, the company belongs to the “manufacturing†“textile industry†“chemical fiber weaving and printing and dyeing finishing†sub-industry (codes 1751, 1752), According to the “Guidelines for the Classification of Listed Companies in the Industry†issued by the China Securities Regulatory Commission in October 2012, the company belongs to the “Textile Industry†in the “Manufacturing Industry†(code C17).

The net proceeds raised by Taihua New Materials will be 550 million yuan for the annual dyeing of 80 million meters of high-grade differentiated functional nylon fabric expansion project, and the finishing of 34.5 million meters of high-grade special functional fabric expansion project, new fiber and fabric technology research and development. Central project.

SFC inquires income growth of 18% net profit growth of 450%

According to the website of the China Securities Regulatory Commission, on August 9, 2017, the Board of Directors of the Board of Directors issued a number of inquiries to Taihua New Materials in the announcement of the results of the 120th meeting in 2017.

1. The issuer's representative is requested to further explain the following matters: (1) Reasons and reasonableness of the significant increase in the gross profit margin of the major products of the issuer in 2016; the issuer's gross profit margin is higher than the average of comparable companies in the same industry. Specific reasons and reasonableness; (2) Reasons and rationality of inconsistent and inconsistent gross margin of the issuer's internal and external sales; (3) The net profit of the issuer fluctuated greatly during the reporting period, and the net profit continued to decline sharply from 2013 to 2015. In 2016, the specific reason and rationality of net profit growth of 450% in the case of only 18.29% of revenue growth; (4) combined with the current orders, 2017 operations, macroeconomic and upstream and downstream industry development, Further explain whether the operating profit of the issuer's listing in the year of the year is more than 50% lower than the previous year or the forecast basis and reason for the loss in the year of listing, whether it is prudent and reasonable, and whether the relevant risks are fully disclosed; (5) Combining raw material price fluctuations, exchange rate fluctuations, and foreign trade policies Changes, downstream apparel industry demand fluctuations, issuer's inventory proportion is relatively high, accounts receivable are higher, issuer's operation in 2017 In terms of performance, etc., further analysis shows whether the issuer's industry status or the operating environment of the issuer's industry has undergone or will undergo major changes, and has a material adverse impact on the issuer's continued profitability. Please sponsor the representative to explain the verification method, procedure, basis and conclusion.

2. The issuer's representative is requested to further explain: (1) the specific reasons and reasonableness of the higher and rising balance of accounts receivable and notes receivable at the end of each period of the reporting period; whether it will adversely affect the issuer's performance and continuing operations. (2) In combination with the credit term and the time of payment after the period, supplement whether the period of the report period stimulates sales through the relaxation of the credit policy; (3) Whether the payment after the period of accounts receivable at the end of each period is in conformity with the issuer Agreement with the customer's credit period; (4) Whether there is a way to adjust the age of accounts receivable through the offset of the third-party company's payment; whether there is external borrowing at the end of the accounting period, and the self-owned funds reduce the accounts receivable, (5) The specific reason for the issuer's provision for bad debts within 6 months of the account, and its reasonableness and compliance; (6) Combining the issuer's receivables at the end of each period The account aging status, the actual write-off of bad debts during the reporting period, and the comparison between the issuer and the bad debt provisioning policies of comparable companies in the same industry, indicating whether the proportion of bad debt provision is cautious and sufficient; (7) No issue there is no real trading background acceptances, discounted notes receivable due to inability, acceptance, and can not be converted due in the case of accounts receivable. Please sponsor the representative to issue a verification opinion.

3. The issuer's representative is requested to further explain: (1) Whether the issuer's production and operation and fundraising projects comply with the national environmental protection and safety production regulations, whether or not to obtain the necessary permit documents such as discharge permits; (2) Report During the period and the current issue of the issuer's environmental protection law and the internal control system construction and implementation of environmental protection, whether it meets the requirements of relevant environmental laws and regulations, national and industrial standards, whether there has been an environmental accident, whether it has been subject to environmental protection authorities (3) Whether the costs related to environmental protection and future expenditures, relevant environmental protection inputs, environmental protection facilities and daily pollution control costs are matched with the pollution generated by the issuer's production and operation during the reporting period; the issuer's discharge and pollution treatment (4) The issuer's revenue increased in 2016, but the issuer's investment in environmental protection equipment decreased from 10,020,300 yuan in 2014 to 1,729,800 yuan in 2016, and 2016 nitrogen oxides, etc. The discharge of major pollutants has a large decline, and whether the above indicators are not comparable The situation; whether there is a situation that increases profits by reducing the cost of environmental protection equipment and facilities; (5) whether the issuer has accepted the verification by the local environmental protection department in accordance with the Notice on Implementing the Comprehensive Pollution Discharge Plan for Industrial Pollution Sources; (6) In February 2016, when an employee accidentally died while operating a forklift, did the issuer have other security incidents during the reporting period, and whether there were administrative penalties for violating the relevant laws and regulations on safety production in the country; Whether the internal control level of safety production is established and effectively implemented. Please sponsor the representative to issue a verification opinion.

4. The issuer's representative is requested to further explain: (1) The issuer's import of raw materials, nylon chips, involves anti-dumping duties, and whether the issuer evades anti-dumping duties by selling to Hong Kong subsidiaries and importing them into the country is a malicious evasion of anti-dumping duties. Whether the situation is in line with China's Customs Law, Import and Export Tariff Regulations, Anti-dumping Regulations, Foreign Exchange Regulations and other relevant laws and regulations; whether there is a risk of being punished and recovered; (2) the issuer is engaged in feeding Whether the processing of nylon filament business has obtained the approval of the competent departments such as business, customs, foreign exchange management, and tax administration; (3) If the anti-dumping duty is to be paid, the specific amount to be paid in each period of the reporting period and the proportion of income and profit Whether it will have a material adverse effect on the issuer's operating performance and continued profitability, and whether it constitutes a substantial legal obstacle to the issuance; whether the relevant information disclosure and risk disclosure are sufficient. Please sponsor the representative to explain the verification method, procedure, basis and conclusion.

In addition, on June 9, 2017, the China Securities Regulatory Commission issued a number of inquiries to Taihua New Materials in the initial application feedback. In February 2016, an employee of the company had an accident while operating the forklift and died after being rescued. Please add: (1) Whether the company has potential safety hazards or major safety production accidents, whether it will affect the issuer's production and operation, whether major safety production accidents occur; (2) Whether the issuer's safety production system is perfect and the safety facilities operate Happening. The sponsor institution and the issuer's lawyer are required to combine the safety accidents occurred during the reporting period, and whether the accidents are major safety production accidents and whether the punishments constitute a major illegal act, and whether the company's internal control system is perfect.

The balance of the issuer's accounts receivable at the end of each period is higher. During the reporting period, the turnover rate of accounts receivable decreased year by year and was lower than the average level of companies in the same industry. Please add in the “Management Discussion and Analysis†section of the prospectus: (1) further explain the reasons for the decline in the turnover rate of accounts receivable, the credit policy of the issuer to the customer, and whether there is a relaxation of the credit policy during the reporting period. (2) According to the credit period and the credit period, the balance of accounts receivable and the age of the accounts are added; (3) The main customers with the balance of the receivables at the end of each period of one year or more and the corresponding amount and age In conjunction with the issuer's credit policy, it further explains the reasons for the unpaid long-term payment, whether there is a risk of payment, and whether the relevant provision for bad debts is sufficient.

The issuer's inventory balance at the end of each period is relatively high, mainly for raw materials, inventory goods and products. Please add in the “Management Discussion and Analysis†section of the prospectus: (1) In the raw materials and stocks at the end of each period, the composition of nylon finished products, nylon filaments, nylon grey fabrics, and the issuer’s nylon filaments for self-production. (6) Whether the supply and sales of nylon finished products, nylon filament yarns, and nylon fabrics are matched with the inventory balance; (3) In the products and stocks at the end of each period, nylon finished products, nylon filaments, nylon fabrics The coverage of the order, the main customers corresponding to the order; (4) the age of raw materials and stocks at the end of each period, combined with the age of the library to further explain whether the issuer's products are slow-moving, and whether the provision for inventory depreciation is sufficient; (5) Reporting period Within, the issuer's accounting method for the inventory depreciation reserve, the accounting basis, the amount of the inventory depreciation loss accrued in each period, the corresponding major assets, the reasons for the accrual, the reason for the substantial increase in the amount of the depreciation loss during the reporting period, the follow-up of the relevant assets Disposal situation, etc.

Bank borrowing accounted for 61.72% of debt, 3 years interest of 271 million

Bank loan situation

According to the prospectus, in recent years, corporate bank borrowings have remained at a relatively high level. From 2014 to January to January 2017, bank loans were 1,581,930,300 yuan, 1,903,596,300 yuan, 1,636,409,900 yuan, 1,364,885,900 yuan, 941,931,500 yuan and 83,344.74 yuan. 10,000 yuan, from 2014 to January-June 2017, the company's corresponding interest expenses were 117,289,900 yuan, 940,100,000 yuan, 5,941,770 yuan and 20,154,200 yuan, respectively, the amount is higher. The proportion of corporate bank borrowings to total liabilities was 71.35%, 70.32%, 61.72% and 55.64%, respectively, which accounted for a relatively high proportion and was a major component of the company's liabilities.

The above data shows that the company's 2014-2016 interest expenses totaled 271 million yuan.

At the end of the reporting period, the company's current ratios were 0.86, 0.87, 0.97 and 1.09, respectively. The quick ratios were 0.43, 0.48, 0.57 and 0.64 respectively. As of June 30, 2017, the company's parent company's asset-liability ratio was 31.39%. The asset-liability ratio is 48.89%, and the company has a certain risk that the debt will not be settled as scheduled.

From 2014 to January-June 2017, the bank loan balance of the company showed a downward trend. At the end of 2015, it decreased by RMB 270.164 million compared with the end of 2014, a decrease of 16.51%. At the end of 2016, it decreased by RMB 416,684,400, a decrease of 30.50% compared with the end of 2015. At the end of the month, it decreased by RMB 115.87 million compared with the end of 2016, a decrease of 12.21%. This was mainly due to the company's strengthening of financial expense management control since 2015, which further returned some long-term loans and short-term loans. As of June 30, 2017, the company did not have bank loans that were overdue.

More than half of the company's land use rights, houses and buildings, machinery and equipment have been used for bank mortgage financing. As of June 30, 2017, the company used land rights for mortgages, houses and buildings, machinery and equipment, and electronics. The net book value of equipment and other assets totaled RMB 915,687,300, accounting for 62.26% of non-current assets.

2016 accounts receivable of 300 million yuan

According to the prospectus, from 2012 to January to January 2017, the company's net accounts receivable were 244,506,300 yuan, 287,321,100 yuan, 382,823,700 yuan, 342,253,700 yuan, 294,495,500 yuan, and 486,606,100 yuan. The proportion of accounts receivable to current assets was 14.88%, 15.14%, 21.34%, 21.45%, 20.48%, and 30.68%, respectively. The accounts receivable turnover rate (times) were 7.87, 6.97, 5.80, 5.23, 6.99, and 6.62, respectively.

At the end of June 2017, the company's accounts receivable increased by 189,100,600 yuan compared with the end of 2015. The sales of major companies in the first half of the year occurred in the second quarter, and no refunds were made in the middle of the year. The amount of accounts receivable during the reporting period was generally relatively high.

The company prompts the risk. In the future, with the expansion of the company's business scale, if the balance of accounts receivable remains high, it will bring certain risks to the company: on the one hand, the higher accounts receivable balance occupies the company's operation. The funds reduce the cash flow generated by the company's operating activities and reduce the efficiency of capital use. On the other hand, once the receivables collection cycle is extended or even bad debts occur, it will have a certain impact on the company's performance and production and operation.

Accounts receivable are not accrued within six months. Net profit is increased by more than 10 million.

Bad debt provision for accounts receivable between the company and comparable companies

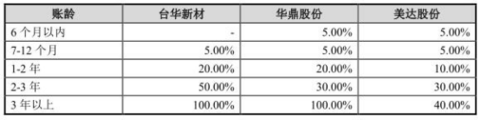

According to the prospectus, compared with comparable companies in the same industry, the company did not make provision for bad debts for accounts receivable within 6 months, mainly because customers who made provision for bad debts according to the ageing combination should be within 6 months. The receivables are not abnormal in terms of estimated recoverable amount; except for accounts receivable within 6 months, the company's other aging accounts receivables are all higher than or equal to comparable companies in the same industry, and for more than 3 years. The accounts receivable are fully accrued for bad debts. In addition, the company will carefully estimate the receivables for some of the three years and make full provision for impairment based on the collectability of the accounts receivable.

As of the end of 2016, the book value of accounts receivable of Taihua New Materials within 6 months was 275.48 million yuan. If the provision for bad debts was made at 5%, the net profit would be reduced by 13.5 million yuan.

From 2014 to 2016, the balance of accounts receivable of comparable company Huading Co., Ltd. was 268,307,400 yuan, 191,271,900 yuan and 335,605,500 yuan respectively. The balance of accounts receivable of Meida shares was RMB 10,502,600, RMB 90,198,800 and RMB 12,288,500 respectively. From 2014 to 2016, the provision for bad debts was higher than that of comparable companies in the same industry, and the company's accounts receivable were more cautious.

According to the prospectus, during the reporting period, the accounts receivable structure was mainly within one year. From 2014 to January-June 2017, the company's accounts receivable ratio within one year were 98.91%, 96.65%, 97.43% and 99.11%, respectively, and the ageing structure was reasonable.

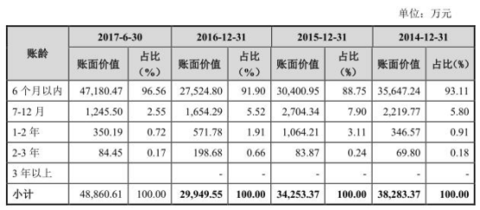

The book value of accounts receivable within 6 months of the company was 356,742,400 yuan, 30,400,500 yuan, 275,488,000 yuan, and 471,184,700 yuan, accounting for 93.11%, 88.75%, 91.90%, and 96.56% respectively.

The book value of the company's accounts receivable from July to December was 22,217,700 yuan, 27,034,400 yuan, 16,552,900 yuan and 12,455,000 yuan, accounting for 5.80%, 7.90%, 5.52% and 2.55% respectively. The book value of the company's accounts receivable for 1-2 years was 3,465,700 yuan, 16,062,100 yuan, 57.178 million yuan, and 3.51 million yuan, accounting for 0.91%, 3.11%, 1.91%, and 0.72%, respectively. The book value of the company's accounts receivable for 2-3 years was 690,800 yuan, 833,700 yuan, 1,868,800 yuan and 844,500 yuan, accounting for 0.18%, 0.24%, 0.66% and 0.17% respectively.

Inventory accounts for 40.85% of current assets.

Company inventory details and proportion of current assets

According to the prospectus, from 2012 to January to January 2017, the book value of the company's inventory was 786,698,600 yuan, 890,958,400 yuan, 892,428,800 yuan, 710,806,500 yuan, 597,365,500 yuan, 666,958,900 yuan, accounting for the proportion of current assets. It is 47.90%, 47.21%, 49.77%, 44.97%, 40.85%, and 41.97%. The inventory turnover rate (times) was 1.70, 1.72, 1.72, 1.86, 2.55, 2.85, respectively.

According to the company, the total proportion of nylon filament and nylon fabrics accounted for more than 70% of the balance of inventory at the end of the reporting period. On the one hand, the company will reduce the inventory of grey cloth as one of the main management objectives. On the other hand, it will increase the development and sales of finished fabrics at the back end of the industrial chain. The digested grey cloth will gradually increase, so the proportion of grey cloth in inventory will decrease year by year.

As of June 30, 2017, the book value of the company's consolidated treasury was 668,594,900 yuan, accounting for 21.82% of the total assets, of which 335,319,900 yuan was inventories, accounting for 49.84% of the inventory. As of June 30, 2017, the company's provision for inventory depreciation was RMB 59,987,700, accounting for 8.22% of the inventory balance. At present, the company has strengthened the management of inventory, but in the future business year, due to changes in the market environment or increased competition, the increase in inventory prices or the difficulty in realizing inventory will adversely affect the company's operating results.

The main products of nylon filament and grey cloth prices have fallen.

The main business income of the company is divided into product composition

Average sales price of the company's main products

According to the prospectus, nylon filament, nylon grey fabric and nylon finished fabric are the main products of the company. The proportion of the three types of products in the main business income remains above 80%.

From 2012 to January-June 2017, the average sales price of nylon filament yarns of the company was 3.04 yuan/kg, 2.63 yuan/kg, 2.34 yuan/kg, 2.16 yuan/kg, 1.87 yuan/kg, 2.20 yuan/kg. The average sales price of nylon grey cloth is 4.39 yuan / meter, 4.23 yuan / meter, 4.14 yuan / meter, 3.77 yuan / meter, 3.66 yuan / meter, 4.31 yuan / meter. The average selling price of nylon finished fabrics was 9.39 yuan / meter, 9.75 yuan / meter, 10.20 yuan / meter, 10.09 yuan / meter, 10.35 yuan / meter, 11.20 yuan / meter.

From 2012 to January to January 2017, the capacity utilization rates of nylon filaments were 97.45%, 97.17%, 99.04%, 90.89%, 99.19%, and 109.43%, respectively. The utilization rate of grey cloth production capacity was 97.50%, 99.13%, 90.79%, 97.52%, 104.24%, and 100.40%, respectively. The dyeing capacity utilization rate of finished fabrics was 81.97%, 96.61%, 97.88%, 97.84%, 99.02%, and 116.34%, respectively. The finished product capacity utilization rate of finished fabrics was 96.52%, 101.87%, 101.45%, 101.60%, 101.93%, and 113.67%, respectively.

Main business gross margin rose

Gross profit margin of each product of the company and its changes

Comparison of gross profit margin of nylon products of listed companies in the same industry

The gross profit margin of the company's polyester products is compared with the above companies

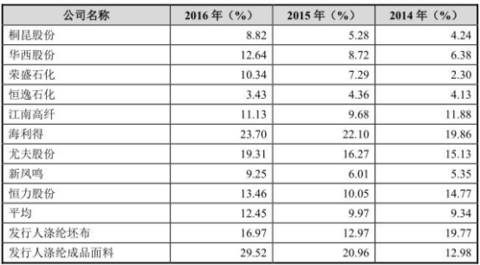

According to the prospectus, from January to June 2017, the gross profit margin of the company's main business was 23.95%, 21.40%, 20.07%, 20.67%, 25.02%, 30.62%. From 2014 to 2016, the gross profit margin of the company's nylon yarn business was 7.19%, 12.44% and 15.69% respectively. The average gross profit margins of related businesses of the peer companies were 8.34%, 9.68%, and 9.89%, respectively. From 2014 to 2016, the gross profit margin of polyester grey cloths was 19.77%, 12.97% and 16.97%, respectively. The gross profit margin of polyester finished fabrics was 12.98%, 20.96% and 29.52% respectively. The average gross profit margins of related businesses of the peer companies were 9.34%, 9.97%, and 12.45%, respectively.

According to the company, due to industry factors, the gross profit margin of the company and the comparable company's nylon yarn business fluctuated from 2014 to 2016. The gross profit rate fluctuation trend of the company's nylon filaments is consistent with the industry average, showing a trend of increasing year by year, and the company's and comparable companies' gross profit margin in 2016 has increased from 2014.

The company's polyester products are mainly polyester fabrics and polyester finished fabrics, while the main products of the above-mentioned polyester industry companies are mostly polyester filaments and their upstream polyester chips and other products with lower gross profit margins, and the gross profit margin is less comparable. Among them, Helide and Yufu's main business income have more than 10% of fabric revenue, and its gross profit margin during the reporting period is significantly higher than that of other polyester industry listed companies, reflecting the gross profit margin of polyester grey fabric and polyester finished fabric downstream of the industrial chain. Relatively high features.

The CSRC issued an inquiry to the gross profit margin of Taihua New Materials in the initial application feedback: During the reporting period, the gross profit margin of the issuer's main products was quite different. The relevant situation of polyester products is not disclosed in the prospectus. Please add in the “Management Discussion and Analysis†section of the prospectus: (1) Gross profit and gross profit margin of domestic and foreign sales in each period of the reporting period, and make a comparative analysis; (2) Income and cost of polyester products in each period , cost structure, gross profit, gross profit margin, etc., and further analysis; (3) combined with the main customers of each polyester product, selling price, pricing basis, raw materials, cost, cost structure, etc., further explain and disclose the issuer's various nylon The difference in gross profit margin between products is large, and the fluctuation trend is inconsistent; (4) further explain that the issuer's nylon yarn business has significantly increased its gross profit margin in 2015 and 2016, and is much higher than that of the same industry company. Reasons for large differences with companies in the same industry.

The actual controller is involved in four guarantee proceedings. 30 million bad debts or difficult to recover

According to Hexun.com, Taihua New Materials and its holding subsidiaries currently have 4 major lawsuits. Among them, 3 cases were dunning suits for accounts receivable between Taihua New Materials and customers, involving a total of approximately RMB 3,148.45 million in non-returnable principal and interest. Shi Qingdao, the company's actual controller, also involved 4 joint guarantee lawsuits, which required a large amount of joint guarantee responsibility, involving an amount of about 31,729,700 yuan.

The prospectus shows that there are 4 major lawsuits involving the company and its holding subsidiaries, as follows:

(1) Litigation of Xiamen Liangyu Trading Co., Ltd. Xiamen Liangyu Trading Co., Ltd. is a customer of the Company. As of April 30, 2013, the parent company Taihua New Materials has received a payment of RMB 20,662,993.20. Due to difficulties in its operations, it is in arrears. On December 19, 2013, the Xiuzhou District People's Court of Jiaxing City issued a judgment ((2013) Jiaxiu Shangchu Zi No. 335 Civil Judgment), and the judgment was issued by Xiamen Liangyu Trading Co., Ltd. and Quanzhou Liangxing Dyeing Flocking Co., Ltd. The company paid the purchase price of RMB 20,662,993.20 and compensated for the loss of interest (based on the 20,662,993.20 yuan basis, according to the benchmark interest rate of the same grade loan announced by the People's Bank of China, from June 1, 2013 to the date of performance as determined by the judgment); The expenses related to property preservation are calculated at RMB 150,114.00 from Xiamen Liangyu Trading Co., Ltd. and Quanzhou Liangxing Dyeing Flocking Co., Ltd.

In November 2014 and January 2017, the parent company Taihua Xincai received RMB 2,459,200 and RMB 1.38 million from Xiamen Liangyu Trading Co., Ltd. As of June 30, 2017, the remaining payment of RMB 16,682,800 has not been recovered, and the company has made full provision for bad debts.

(2) Litigation of Zhejiang Zhuangchi Industrial Co., Ltd. Zhejiang Zhuangchi Industrial Co., Ltd. is a customer of the company. As of December 31, 2013, the subsidiary Fuhua Fabrics received a payment of RMB 7,671,180.08. Due to difficulties in its operations, it is in arrears. On April 2, 2015, the Suzhou Intermediate People's Court made a judgment ((2014) Su Zhong Shang Chu Zi No. 00141 Civil Judgment), and the judgment was paid by Zhejiang Zhuangchi Industrial Co., Ltd. to the company for 7,671,180.08 yuan and compensated for interest losses ( Based on the 7,671,180.08 yuan, according to the benchmark interest rate for the same grade loans announced by the People's Bank of China, from September 5, 2014 to the date of performance as determined by the judgment, Zeng Taiwen assumed the corresponding joint liquidation responsibility.

In 2016, the subsidiary Fuhua Fabric received RMB 810,619.00 from Zhejiang Zhuangchi. As of June 30, 2017, the remaining 6,628,139.08 yuan and the corresponding interest have not been recovered, and the company has made full provision for bad debts.

(3) Litigation of Hubei Kael Garment Co., Ltd. and Guangdong Qiulu Industrial Co., Ltd. Hubei Kael Garment Co., Ltd. is a customer of the company. Due to the dispute between Hubei Kael Garment Co., Ltd. and its customers, the company has defaulted on the payment. On June 13, 2016, the People's Court of Xiuzhou District of Jiaxing City issued the Civil Judgment ((2015) Jiaxiu Shangchu No. 106), and determined that Hubei Kael Garment Co., Ltd. paid high-tech within 10 days from the effective date of the judgment. Dyeing and fixing the purchase price of 6,551,112.5 yuan and compensating for the loss of interest on overdue payment, Guangdong Qiulu Industrial Co., Ltd. shall bear the joint liquidation responsibility for the above debts. The payment can be deducted from the payment of the payment to Guangdong Qilu Industrial Co., Ltd. by the customers of Guangdong Qiulu Industrial Co., Ltd. .

As of June 30, 2017, the company's subsidiaries have not recovered their receivables, and the company has made full provision for bad debts.

(4) Litigation of Zhejiang Xiangda Construction Co., Ltd. On July 15, 2013, Gaoxin Dyeing and Finishing and Sugawara Construction Group Co., Ltd. (hereinafter referred to as “燎原公å¸â€) signed a contract for the renovation of circulating fluidized bed boiler project. The company has rebuilt the high-tech dyeing and finishing boiler project with a total contract value of 1,000. Ten thousand yuan. On December 22, 2014, Liaoyuan Company transferred the creditor's right of Gaoxin Dyeing and Finishing to its tail payment of RMB 3 million to Zhejiang Xiangda Construction Co., Ltd. (hereinafter referred to as “Zhejiang Xiangdaâ€). On December 23, 2014, Zhejiang Xiangda sent a notice of transfer of creditor's rights and a creditor's rights transfer agreement to Gaoxin Dyeing and Finishing. Gaoxin Dyeing and Finishing filed an objection to Zhejiang Xiangda on December 25, 2014, and verified the transfer of the above-mentioned creditor's rights to Liaoyuan Company. On February 11, 2015, Liaoyuan Company sent a letter to Gaoxin to confirm that the project was still under the contract. All the disputes caused by the payment to the company are borne by the company. On November 16, 2015, Zhejiang Xiangda filed a lawsuit against the Xiuzhou District People's Court of Jiaxing City, requesting that the high-tech dyeing and payment payment be 3 million yuan, and compensation for interest losses and litigation costs.

International Finance News: Taihua New Materials' net profit surged three major financial technologies

According to the "International Finance News" report, the prospectus disclosed that from 2014 to 2016, Taihua New Materials realized operating income of 1.942 billion yuan, 1.879 billion yuan and 2.244 billion yuan respectively, and the net profit for the same period was 80.604 million yuan and 41.395 million yuan respectively. 2.28 billion yuan.å°åŽæ–°æ2016年净利润较2015年净增1.88亿元,åŒæ¯”暴增449.71%。

å°åŽæ–°æçªç„¶æš´å¢žçš„净利润从何而æ¥ï¼Ÿã€Šå›½é™…金èžæŠ¥ã€‹è®°è€…查阅招股说明书åŽå‘现主è¦æ¥æºäºŽä»¥ä¸‹ä¸‰ä¸ªæ–¹é¢ã€‚

其一,主è¥ä¸šåŠ¡äº§å“æ¯›åˆ©çŽ‡çš„å¢žåŠ ã€‚æ•°æ®æ˜¾ç¤ºï¼Œ2015å¹´è¥ä¸šæ”¶å…¥è¾ƒ2014 年略有下é™ï¼Œ2015 年毛利é¢ä¸Ž 2014 年基本æŒå¹³ã€‚å°åŽæ–°æ表示,éšç€ä¸Šæ¸¸çŸ³æ²¹ä»·æ ¼çš„回å‡ï¼Œä¸”å…¬å¸ç§¯æžè°ƒæ•´äº§å“和客户结构,2016å¹´å…¬å¸çš„毛利率åŒæ¯”å¢žåŠ ã€‚ç”±äºŽæ¯›åˆ©çŽ‡åŒæ¯”å¢žåŠ 4.27%,å°åŽæ–°æ2016 年的毛利é¢åŒæ¯”å¢žåŠ äº†1.68亿元。

其二,财务费用的大幅å‡å°‘。å°åŽæ–°æ毛利率的æé«˜ï¼Œå¢žåŠ äº†å…¬å¸çš„毛利é¢ï¼Œä»Žè€Œå½±å“到净利润。而财务费用的大幅å‡å°‘åˆ™æ›´åŠ ç›´è§‚åœ°å½±å“了净利润。å°åŽæ–°æ表示,报告期内公å¸æŒç»å¿è¿˜é“¶è¡Œå€Ÿæ¬¾ï¼Œå…¬å¸åˆ©æ¯æ”¯å‡ºæŒç»ä¸‹é™ï¼›ç”±äºŽæŠ¥å‘ŠæœŸå†…汇率æŒç»å˜åŒ–,汇兑æŸç›Šä¹Ÿå˜åœ¨æ³¢åŠ¨ã€‚招股书指出,2015 年下åŠå¹´å¼€å§‹ç”±äºŽæ—¥å…ƒå…‘人民å¸æ±‡çŽ‡ä¸Šå‡ï¼Œå…¬å¸å¤–å¸å€Ÿæ¬¾æ±‡å…‘æŸå¤±å¢žåŠ 较多。数æ®æ˜¾ç¤ºï¼Œå…¬å¸æŠ¥å‘ŠæœŸå†…的利æ¯æ”¯å‡ºå’Œæ±‡å…‘æŸç›Šï¼ˆä¸åŒ…括利æ¯æ”¶å…¥å’Œæ‰‹ç»è´¹æ”¯å‡ºï¼‰ä¸¤é¡¹åˆè®¡åˆ†åˆ«ä¸º 10944.61 万元ã€11907.57 万元和 7044.72 万元,2015年较2014å¹´å¢žåŠ 962.96万元,2016年较2015å¹´å‡å°‘4862.85 万元,该项财务费用直接影å“了公å¸çš„å‡€åˆ©æ¶¦ï¼Œé€ æˆä¸šç»©æ³¢åŠ¨ã€‚

其三,资产å‡å€¼æŸå¤±å¤§å¹…é™ä½Žã€‚å°åŽæ–°æ在解释净利润波动时也æ到了资产å‡å€¼æŸå¤±æŠ¥å‘ŠæœŸå†…,公å¸å„期å‡æœ‰ä¸€å®šçš„资产å‡å€¼æŸå¤±ï¼Œèµ„产å‡å€¼æŸå¤±çš„波动也是净利润波动的主è¦åŽŸå› 之一。招股书显示,报告期内资产å‡å€¼æŸå¤±ä¸ä¸»è¦ä¸ºå˜è´§è·Œä»·æŸå¤±ï¼Œèµ„产跌价æŸå¤±çš„波动对公å¸åˆ©æ¶¦çš„波动也产生了较大影å“。其ä¸2015年较2014å¹´å¢žåŠ äº†2624.11万元,2016年较 2015 å¹´å‡å°‘ 3133.25 万元。

值得注æ„的是,高é¢çš„净利润主è¦ä¾é 财务费用和资产å‡å€¼æŸå¤±çš„大幅é™ä½Žã€‚业内人士表示,å°åŽæ–°æ业绩如æ¤æš´å¢žï¼Œä½†å®žé™…ç»è¥çŠ¶å†µçš„改善并ä¸æ˜Žæ˜¾ï¼Œå¦‚果其æˆåŠŸä¸Šå¸‚,很å¯èƒ½é¢ä¸´ä¸šç»©çŸæœŸç¿»è„¸çš„风险。

上市å‰ä¸‰å¹´ç´¯è®¡åˆ†çº¢6240万元

招股书显示,2012 年至今,公å¸è¿›è¡Œè¿‡ 3 次利润分é…,具体情况如下:

2015 å¹´ 3 月 31 日,公å¸å¬å¼€ 2014 年度股东大会,审议通过了《关于 2014年度利润分é…åŠèµ„æœ¬å…¬ç§¯é‡‘è½¬å¢žè‚¡æœ¬çš„è®®æ¡ˆã€‹ï¼Œå†³å®šä»¥å…¬å¸ 2014 年末总股本48,000 万股为基数,å‘å…¨ä½“è‚¡ä¸œæ¯ 10 è‚¡æ´¾å‘现金红利 0.3 元(å«ç¨Žï¼‰ï¼Œå…±æ”¯ä»˜çº¢åˆ© 1,440 万元。

2016 å¹´ 3 月 18 日,公å¸å¬å¼€ 2015 年度股东大会,审议通过了《关于 2015年度利润分é…åŠèµ„æœ¬å…¬ç§¯é‡‘è½¬å¢žè‚¡æœ¬çš„è®®æ¡ˆã€‹ï¼Œå†³å®šä»¥å…¬å¸ 2015 年末总股本48,000 万股为基数,å‘å…¨ä½“è‚¡ä¸œæ¯ 10 è‚¡æ´¾å‘现金红利 0.3 元(å«ç¨Žï¼‰ï¼Œå…±æ”¯ä»˜çº¢åˆ© 1,440 万元。

2017 å¹´ 4 月 11 日,公å¸å¬å¼€ 2016 年度股东大会,审议通过了《关于 2016年度利润分é…åŠèµ„æœ¬å…¬ç§¯é‡‘è½¬å¢žè‚¡æœ¬çš„è®®æ¡ˆã€‹ï¼Œå†³å®šä»¥å…¬å¸ 2016 年末总股本48,000 万股为基数,å‘å…¨ä½“è‚¡ä¸œæ¯ 10 è‚¡æ´¾å‘现金红利 0.7 元(å«ç¨Žï¼‰ï¼Œå…±æ”¯ä»˜çº¢åˆ© 3,360 万元。

Men'S Ring,Hip Hop Rings,Mens Hip Hop Rings,Hip Hop Silver Rings

Guangzhou Forever Star Jewelry Limited Company , https://www.iforeverstar.com